Fast-growing digital and tech companies generated a lot of investor excitement over the past decade, not to mention an outsized share of market returns.

Since the start of 2022, however, many of these market darlings have taken a beating. Amid slowing economic growth, soaring inflation and the fear of rising interest rates, investors may be taking a second look at the high valuations many digital platform and software stocks command.

“This is one of the most complex environments for investing we have seen in years,” says equity portfolio manager Jonathan Knowles. “With questions lingering over the persistence of inflation and shifts in the geopolitical landscape, I am looking to invest in an ‘all weather portfolio’ with the potential to withstand a variety of potential risks.”

That’s why boring is beautiful according to Knowles. “I’m looking to invest in dull and dependable companies with the potential to generate solid cash flows and continue growing regardless of the direction of the economic cycle or macroeconomic developments.”

Here are some investment themes that cautious investors may want to consider.

Railroads are riding a commodities boom

You can’t build the new economy without old industries.

Long-term shifts toward a digital future, the rollout of electric vehicles and the transition to clean energy will likely continue to drive opportunity for innovators in those areas. But these trends are also providing tailwinds for old industries like mining and railroads.

Nickel, for example, is a key component in electric vehicle batteries. So is copper, which is necessary for updating the electric grid. And while software is becoming an increasingly essential player in the production of modern cars, steel remains a required component. Indeed, prices for select commodities have skyrocketed in recent months, a trend amplified by the war between Russia and Ukraine — major producers of nickel, copper and grains.

“People have underappreciated how much copper is needed to rewire and modernize the electric grid as demand rises,” says equity portfolio manager Andrew Suzman. “Businesses like Canadian metals and mining company First Quantum Minerals, which focuses on copper, and Brazil’s Vale, a producer of iron ore, could benefit.”

Rising demand for commodities and energy could also boost demand for North America’s railroads, which are the most cost-effective way to transport heavy materials. Railroads have pricing power potential as well, which is important in today’s inflationary environment. They typically base their pricing on the cost of the underlying commodities they are hauling, so revenues rise with commodity prices.

Rising fuel costs also prove beneficial, as the difference between the cost of trucking and rails is at its widest gap in years. “A railroad like Canadian Pacific, which has the only tri-coastal Canada-U.S.-Mexico network, could do well under a variety of economic circumstances,” Suzman adds.

Railroads have room to increase pricing amid a commodities boom

Sources: Capital Group, Association of American Railroads, U.S. Bureau of Transportation. Data shown from January 1990 through December 2018. The rail category refers to Class 1 rail, or carriers earning more than $505 million in annual revenue. Pricing per ton-mile refers to the pricing charged for transporting one ton of freight across one mile.

Industrials help power an energy-efficient future

The global push to reduce carbon emissions and improve energy efficiency is often associated with electric vehicles or utilities harnessing solar and wind power. At first blush, traditional industrial companies making machinery, chemicals and other construction materials might be construed as part of the problem, not the solution.

But HVAC companies like Carrier and Daikin are developing air conditioning and heating systems that could help reduce global greenhouse gas emissions. Regulations in Europe and elsewhere that require the replacement of older systems with more energy-efficient products could drive long-term opportunity for both companies.

Tighter carbon emissions regulations and infrastructure spending across major economies could also provide tailwinds for Swiss specialty chemical maker Sika, Knowles says. “The company makes cement additives that can reduce carbon emissions and increase durability,” Knowles says. “This may sound like a boring business, but its growth potential is pretty compelling as global emissions standards tighten.”

Tightening emissions regulations are generating opportunity for select industrials

Sources: Capital Group, company reports, Refinitiv Datastream. Company market capitalizations are in USD as of 3/31/22.

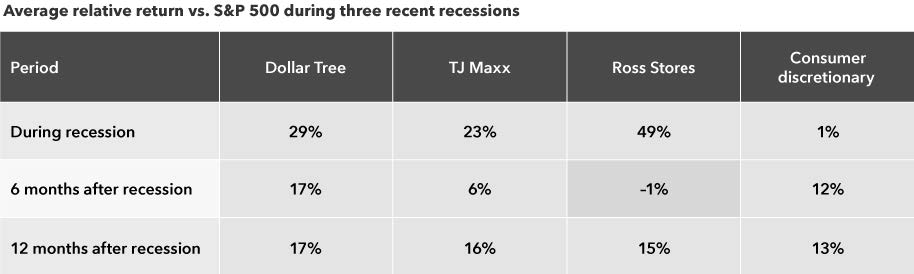

Bargain hunters find “treasure” at dollar stores

When economic conditions become challenging, consumers may naturally become more careful about spending. Many shoppers shift their spending to discount merchants known as treasure hunt retailers. These stores offer clothing, personal care items and household products at relatively low prices, as well as some higher quality products at bargain prices.

“In a slowing economic environment, many people will be trading down to dollar stores,” says portfolio manager Diana Wagner. “Such stores have held up well in past recessions.”

Treasure hunt retailers have outpaced the market in recessions

Source: Capital Group, National Bureau of Economic Research, Refinitiv Datastream, Standard & Poor’s. Reference periods for recessions are March 2001 to October 2001, December 2007 to May 2009, and February 2020 to March 2020. Consumer discretionary category refers to the S&P 500 Consumer Discretionary Index.

What might be less intuitive is that well-run treasure hunt retailers often have pricing power potential when inflation is rising.

For example, Dollar Tree, which offers a wide variety of items for $1, recently launched their “breaking the buck” strategy. The company initially offered a $5 category of goods, followed by a category for $1.25. “This same approach has helped other treasure hunt retailers generate multiple years of strong same-store sales growth and margin expansion,” Wagner says.

A change in senior management at the company could prove to be another tailwind. “Dollar Tree has been undermanaged relative to its competitor Dollar General,” Wagner observes. “But recently Rick Dreiling, the former CEO of Dollar General, was named chairman of Dollar Tree. I think this could be an important turning point for the company.

“In today’s environment, I look for companies that can improve their businesses and make their own growth happen regardless of what the economy does,” Wagner explains. “Dollar Tree could be one of those self-help stories.”

The bottom line

Investors may be wondering if the digital transformation has run its course. “Not at all,” Knowles says. “Leading digital platform companies, cloud software and autonomous vehicle technology continue to reshape the way we work, live and shop. But many of these companies may have gotten ahead of themselves.”

With inflation rising and the earnings potential for many of these companies still years away, valuations may be extended. “Leading technology companies continue to look promising over the long term,” Knowles says. “But in this environment, I am shifting my focus a bit toward companies that actually make stuff and tend to hold their ground during all types of market

weather.”

________________________________________________________________

Jonathan Knowles is an equity portfolio manager with 29 years of investment experience. He has an MBA from INSEAD, France, as well as a PhD in immunovirology and a bachelor’s in

veterinary science from the University of Liverpool, U.K.

Andrew Suzman is an equity portfolio manager with 27 years of investment experience. He holds an MBA from Harvard and a bachelor’s in political economy from Tulane.

Diana Wagner is an equity portfolio manager with 23 years of investment experience. She holds an MBA from Columbia Business School and a bachelor’s degree in art history from Yale

University.

_________________________________________________________________

Investing outside the United States involves risks, such as currency fluctuations, periods of

illiquidity and price volatility, as more fully described in the prospectus. These risks may be

heightened in connection with investments in developing countries.

S&P 500 Index is a market capitalization-weighted index based on the results of approximately

500 widely held common stocks.

The S&P 500 Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and

has been licensed for use by Capital Group. Copyright © 2022 S&P Dow Jones Indices LLC, a

division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in

whole or in part is prohibited without written permission of S&P Dow Jones Indices LLC.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or

any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and summary

prospectuses, which can be obtained from a financial professional and should be read

carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date

published and do not necessarily reflect the opinions of Capital Group or its affiliates. This

information is intended to highlight issues and should not be considered advice, an

endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an

affiliated company or fund. All other company and product names mentioned are the property

of their respective companies.

Use of this website is intended for U.S. residents only.

American Funds Distributors, Inc., member FINRA.

This content, developed by Capital Group, home of American Funds, should not be used as a

primary basis for investment decisions and is not intended to serve as impartial investment or

fiduciary advice.